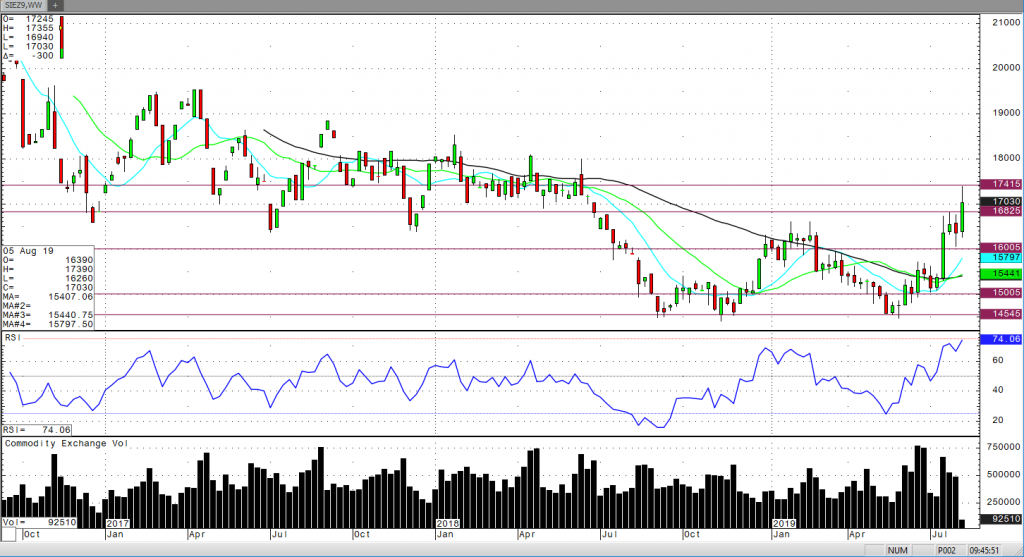

Let’s be real, the rally in gold over the past few weeks has legs this time! My last call on gold was that if we broke the $1460 contract high that a level of $1500 was likely. This was true and then some! The next target for October gold is $1600. Let’s start by looking at the technicals of the contract. The August 1st low is a textbook key reversal; however, it was not validated by a close higher the following session. This didn’t seem to matter as gold has now crossed the psychological $1500 level. The August 7th high volume blowout to the upside is obviously a positive. Yesterday’s October gold traded inside of that previous day’s range and even today as are trading once again in the same range. This contract is likely to move beyond the August 1st range up or down as we consolidate and coil for the next “move.”

Fundamentally, I don’t think there are two market conditions that firmly cement the bull case. The first, obviously, a never-ending trade war with China that is bringing prolonged uncertainty to the markets and thus driving safe haven demand. The second is what appears to be a slowing global economic situation, primarily in Europe. Weak German economic data and the surprise (first in 7 years) decline in the UK GDP data showing their economy contracted .2% this quarter. US economic data has been steady, but with growth likely to slow as we continue to expand tariffs on China gold demand should only get stronger. Let’s not forget the perma-bulls that have now jumped in and are long and strong as we finally break out to new contract high territory relatively speaking. If you would like discuss trade opportunities and ways to structure an October gold trade please contact me directly.