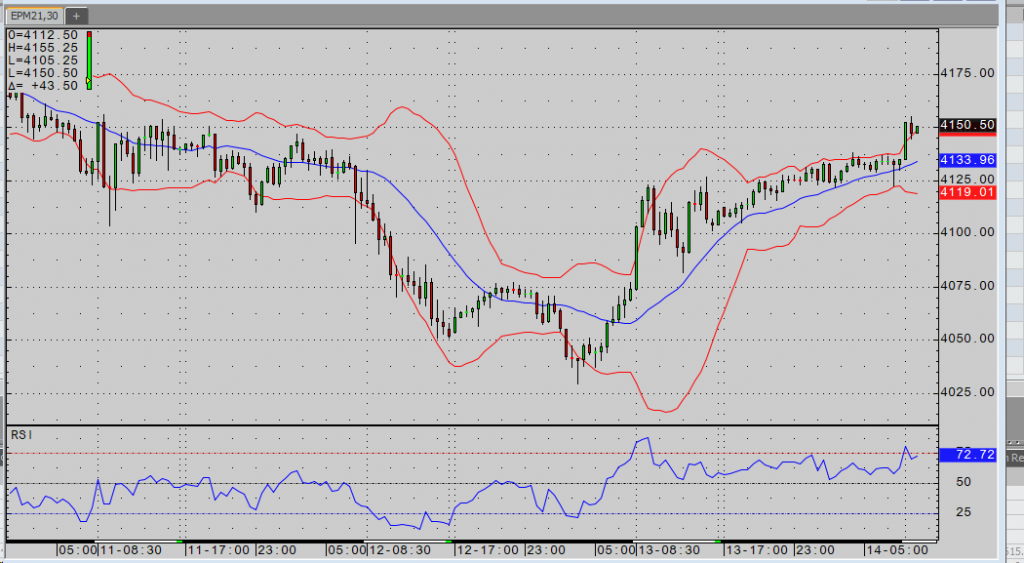

After printing new lows for the move in all four indices yesterday, they all managed to close in positive territory. That momentum has carried into today as all four are currently up anywhere from 0.9% to 1.8%. Inflationary concerns are largely being blamed for the selloff, but you also had Janet Yellen comment that stock valuations “Generally are quite high” earlier in the month. She went on to suggest interest rates may need to rise to prevent the economy from “overheating.” Upon receiving some flack for the comments, she walked them back later in the week. We also saw the Fed warn of the possibility of significant corrections as asset prices continue to climb. While the Fed suggests these inflationary pressures are transitory, Wednesday’s CPI reading of 4.2 percent certainly raised some eyebrows.

Today’s retail sales figure came out unchanged from last month. We had expected to see an increase of one percent. Consumer sentiment missed by a pretty wide margin, coming in at 82.8 vs. an expected reading of 90.3. Next week’s news slate is relatively light. We’ll see a few housing numbers and the weekly jobless claims number, but traders will be looking ahead to the Q1 GDP reading on the 27th.