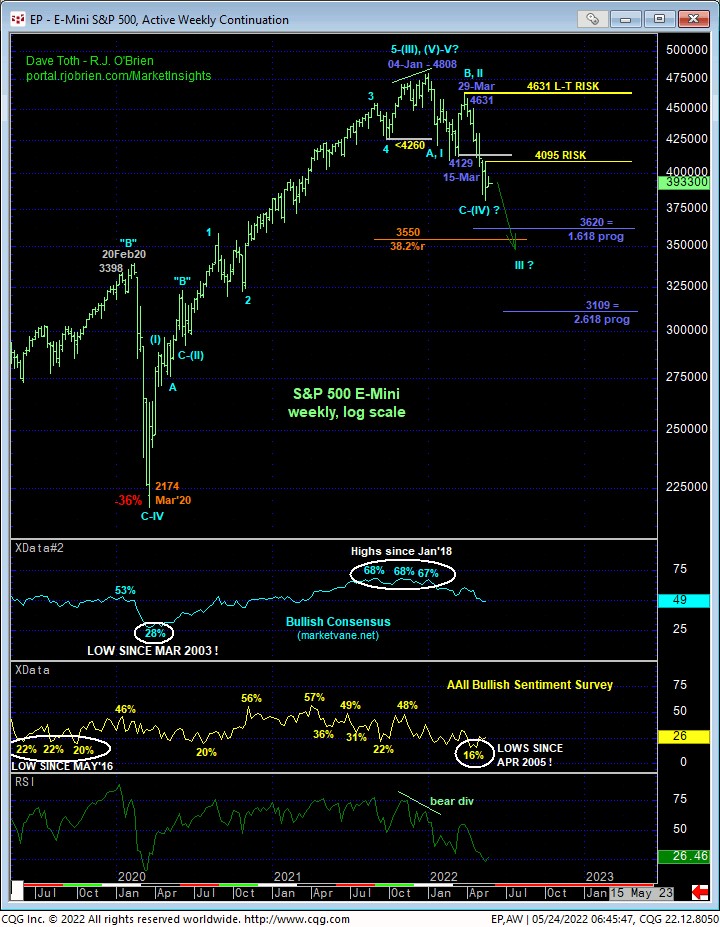

In Fri’s Technical Blog we identified that day’s 3950 high as the latest smaller-degree corrective high the market needed to sustain losses below in order to maintain a more immediate bearish count. The 240-min chart below shows the market’s recovery above this level yesterday, confirming a bullish divergence in short-term momentum. This short-term mo failure defines Fri’s 3807 low as one of developing importance and a short-term risk parameter from which shorter-term traders with tighter risk profiles can objectively base non-bearish decisions like short-covers and cautious bullish punts. Against the backdrop of the major bear trend however, this momentum failure is of too minor a scale to conclude anything more than another interim corrective hiccup ahead of the resumption of the major bear.

On a longer-term scale pertinent to longer-term institutional players and investors, commensurately larger-degree strength above 18-May’s 4095 next larger-degree corrective high remains minimally required to arrest even the portion of the major bear market from 29-Mar’s 4631 high, let alone threaten this year’s entire 20% plunge and major bear market from 04-Jan’s 4808 all-time high. Per such, this 4095 level remains intact as our bear risk parameter from which longer-term players remain advised to maintain and manage the risk of a still-advised bearish policy and exposure. In lieu of a recovery above 4095, further and possibly steep, accelerated and potentially relentless losses that could span quarters remain expected. Needless to say, a relapse below 3807 mitigates yesterday’s bullish divergence in short-term momentum, reinstates the secular bear and exposes potentially sharp losses thereafter.

In sum, yesterday’s bullish divergence in short-term momentum provides the evidence for shorter-term traders with tighter risk profiles to pare or neutralize bearish exposure and perhaps even take a punt from the bull side with a relapse below 3807 negating this call and reinstating the major bear that would require a return to a bearish policy. A bearish policy and exposure remain advised for longer-term players with a recovery above 4095 required to defer or threaten this call enough to warrant moving to a neutral/sideline position. In effect, we believe this market has defined 4095 and 3807 as the key directional flexion points heading forward.