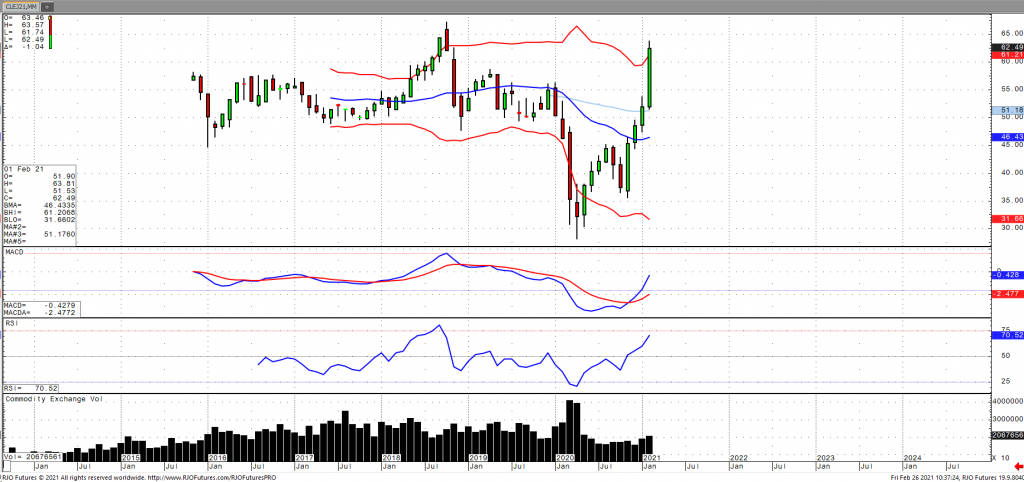

Platinum has been the best performing precious metal over the past four months. We have to pay attention to what’s going on in this metal. Platinum has been beat down versus gold for too long. I want to bring your attention back to November 9th 2020. That was the LOW in platinum. The low in platinum on that day was $851.00 per ounce. April gold low on that same day was $1,859.60 per ounce. The differential on that day was $1,008, gold over platinum. Since then platinum has rallied 63%! Today the differential is at $552. Platinum’s discount to gold is what made it so attractive to money managers and experienced commodity traders that recognized that platinum was severely under-valued at $1,000 under gold. But there’s more to platinum than a “proxy” for gold. Industrial demand has further fueled platinum’s rally. Its use in catalytic converters is widely known and demand for vehicles has increased as signs of the economy growing cannot be ignored. More importantly is future demand for clean energy. Hydrogen power. Hydrogen fuel cell electric vehicles are the future and all the auto makers are getting on board. Platinum will be in much greater demand for those vehicles.

Platinum is still a very good value at $1,200. Metals are already in the beginning of a major bull market. Inflation will be added support after we embrace the fact that interest rates are also rising. Metals are dipping right now because interest rates have risen too fast. Platinum has been ignored for too long. Future demand will drive platinum back towards $2,000. It’s been there before; it won’t be that hard to get back to $2,000.