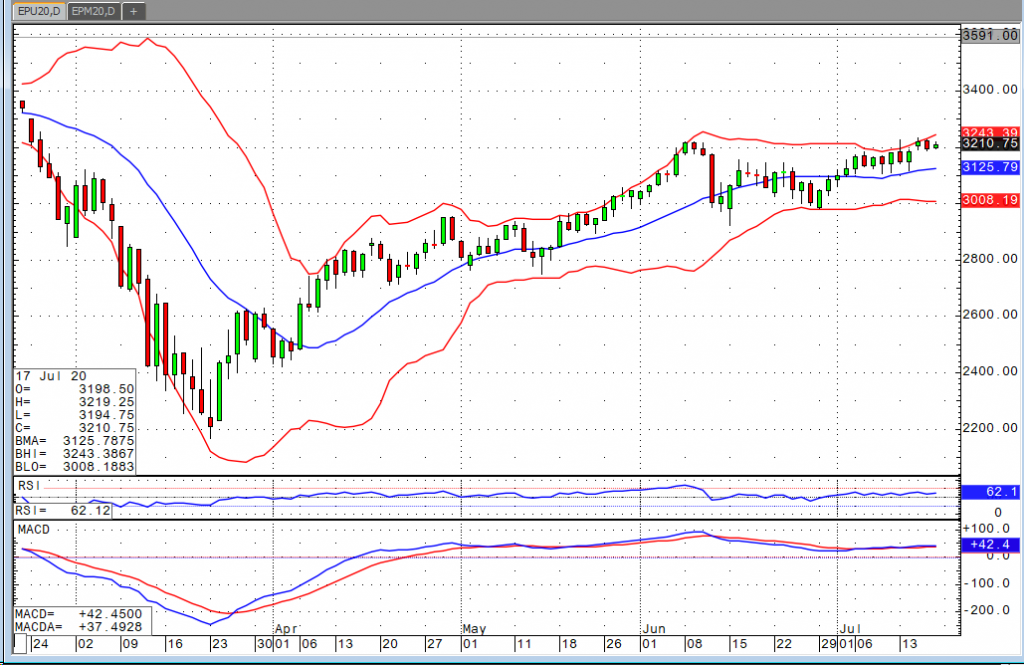

The indices are all up about half a percent or more in the morning’s early stages. Earnings, Covid, and China continue to dominate the headlines. Covid cases are exploding. While we’ve learned a good deal over the past four or five months about who is most at risk, what we can do to try and prevent contracting and/or spreading the disease, we are not seeing the downturn we had hoped for. There are several reasons for this, but I’m not really looking to go down that road here. Depending on the narrative you want to follow, you can find reasons to be optimistic or pessimistic. What matters here though is that the market continues to discount the threat. We’ve seen new highs for the recovery in the S&P and new all-time highs for the Nasdaq this week. Despite this, it is safe to say there is increasing cause for concerns as we’re hearing talks of reversals of re-openings (Gov Abbot has shot down the idea for Texas), schools not opening in the fall, etc. The market seems optimistic about vaccine prospects, but if businesses are going to have to continue to operate below capacity, the market will have to acknowledge that at some point. We saw that on Monday when California announced it was tightening back up, but the dip buyers got paid yet again.